A Concept: Decentralized Super Apps for Emerging Markets

Introduction

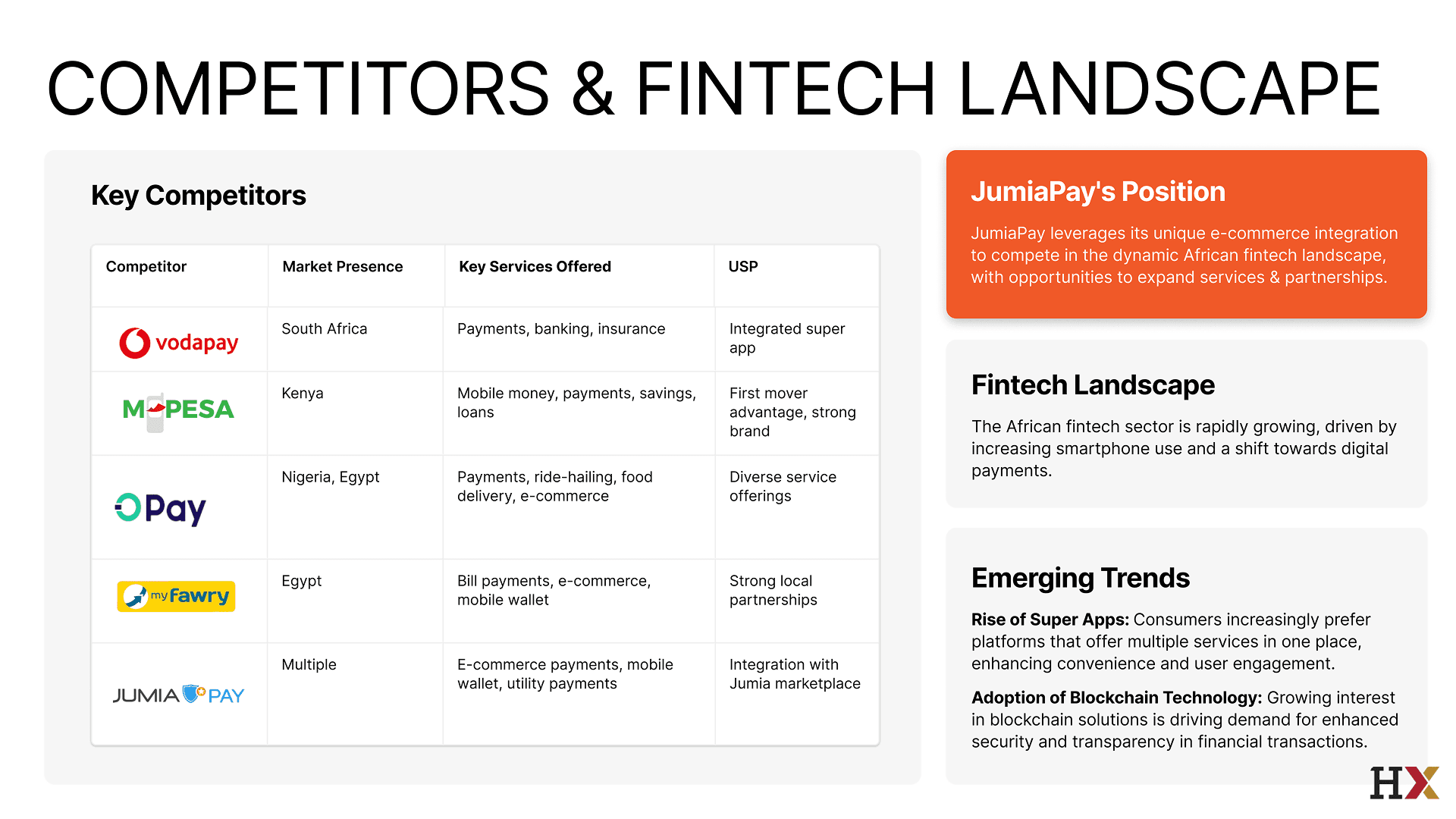

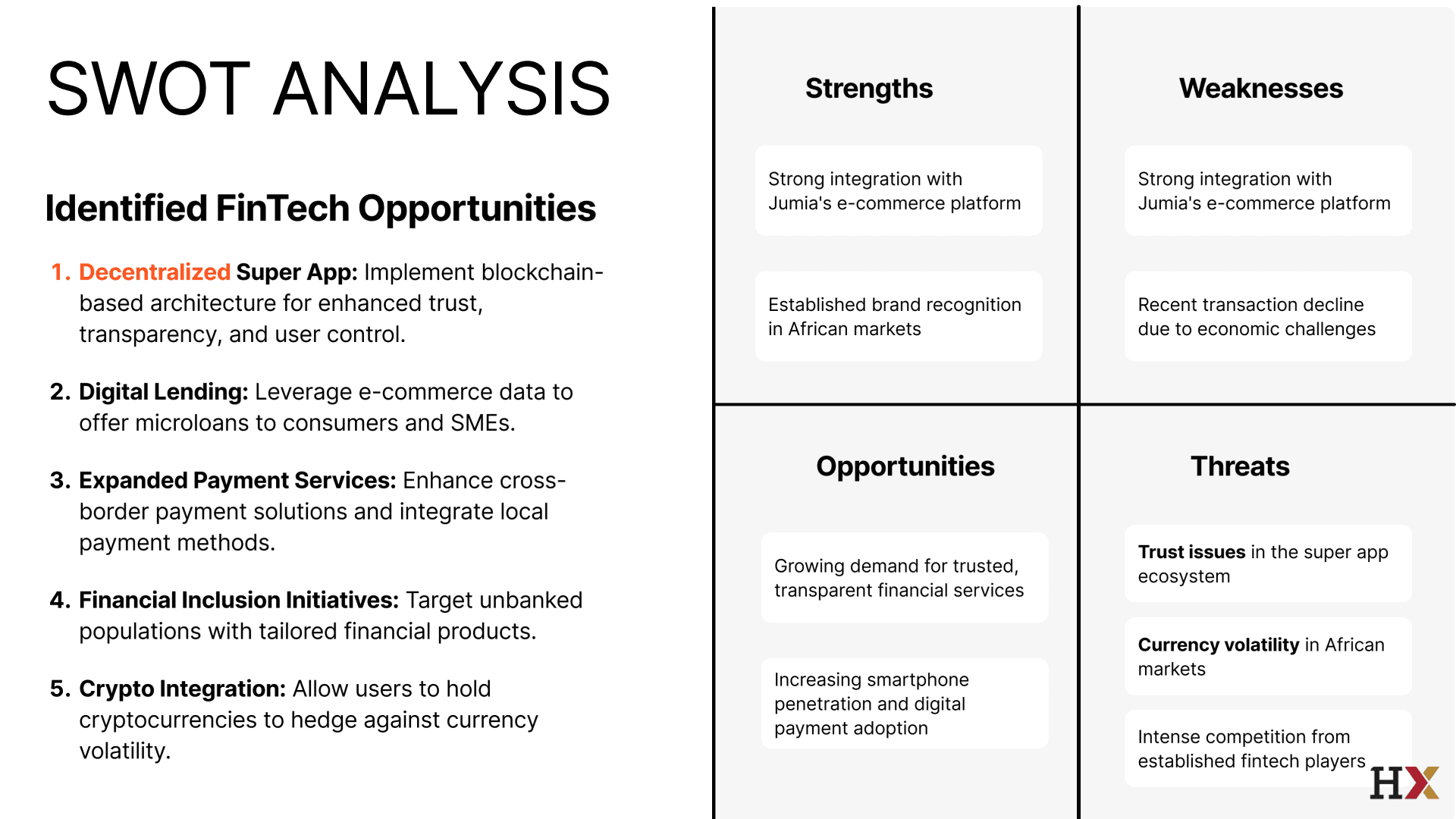

The African fintech landscape is experiencing rapid growth, driven by increasing smartphone penetration and a rising demand for digital payment solutions (Smith, 2022, p. 45). Jumia, often called the “Amazon of Africa” (Doe, 2021, p. 12), has positioned JumiaPay to address this transformation. However, Jumia faces fierce, fast-paced competition and complex economic conditions, including currency volatility, diverse regulatory landscapes, and consumer wariness regarding trust and transparency.

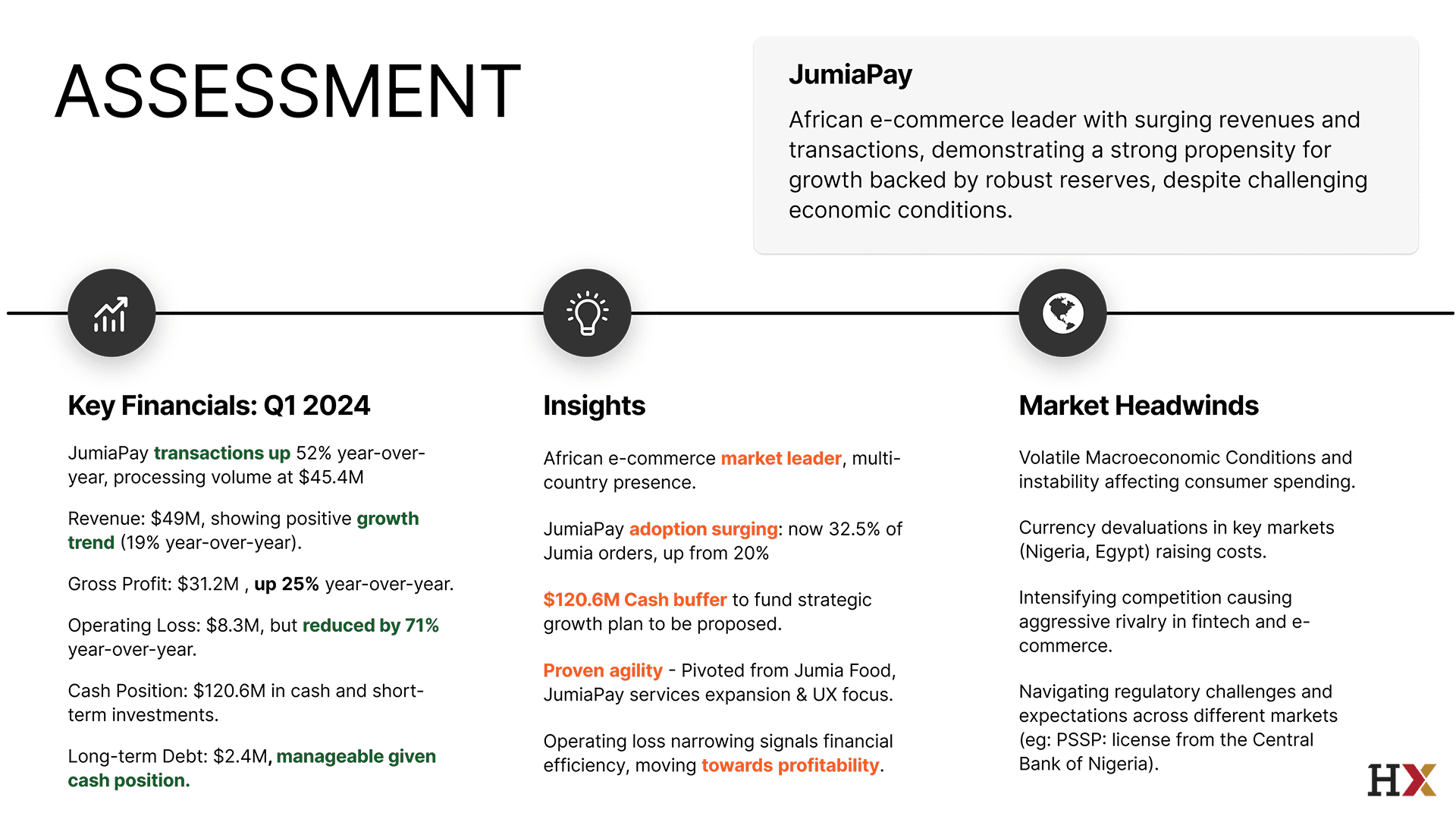

Despite these challenges, JumiaPay is a leader in the space. In Q2 2023, they recorded a total payment volume of $74.2 million, representing 31% year-over-year growth, with 3.4 million transactions processed (JumiaPay, 2023, p. 8). To sustain this growth and maintain market share and influence, they must evolve proactively.

Recommendation: Decentralized Super App

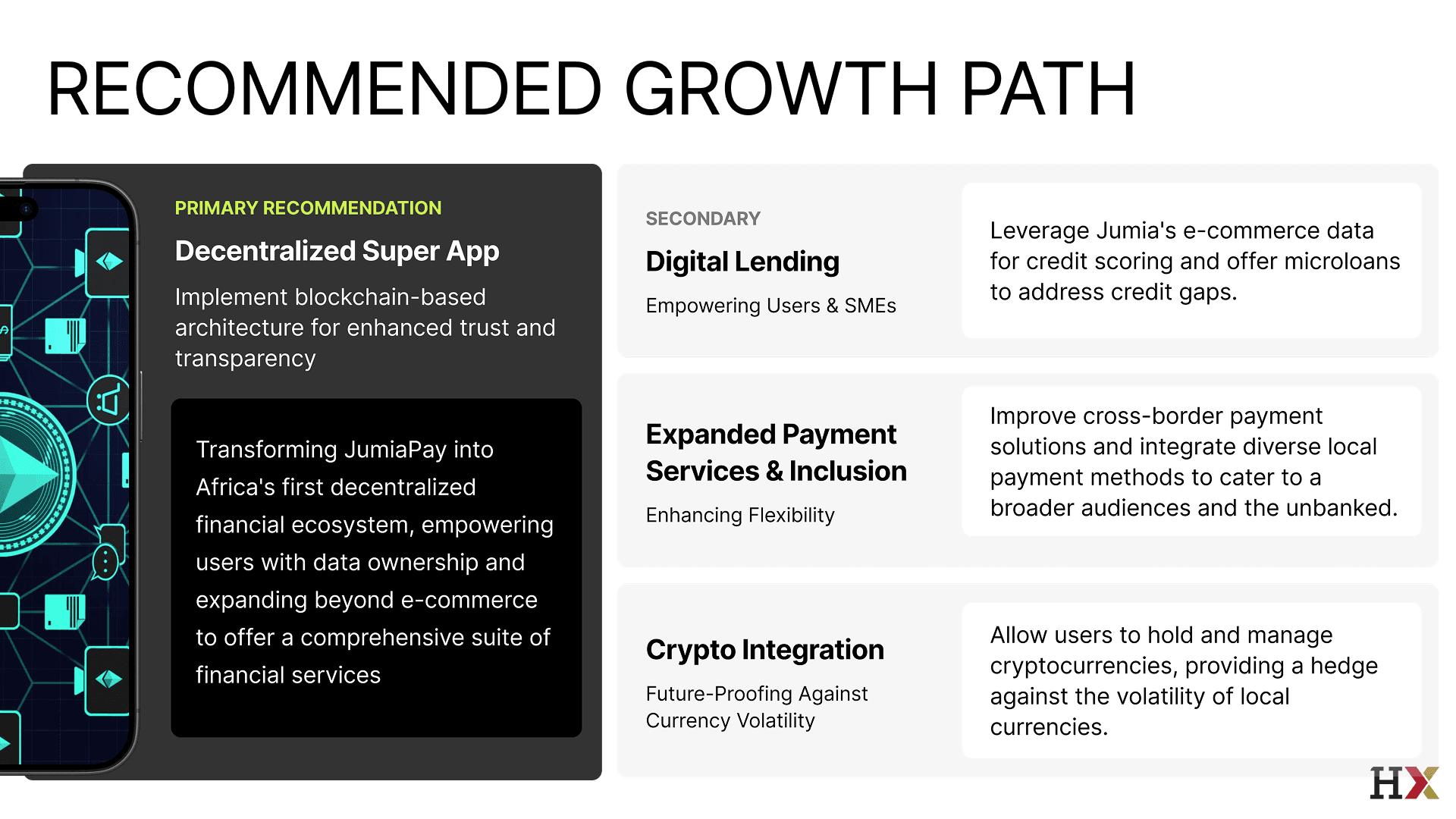

My primary recommendation is to implement a decentralized super app, leveraging blockchain technology to enhance transparency, foster trust, educate communities with the right go-to-market strategy, and potentially mitigate currency risks.

As a super app, JumiaPay integrates various services into a single platform, including e-commerce, food delivery (JumiaFood), travel booking, and payment solutions. This integration is essential for emerging markets like Africa, where users often face barriers such as limited access to banking infrastructure and fragmented service offerings. By consolidating multiple services into one app, JumiaPay simplifies user experiences and drives higher engagement.

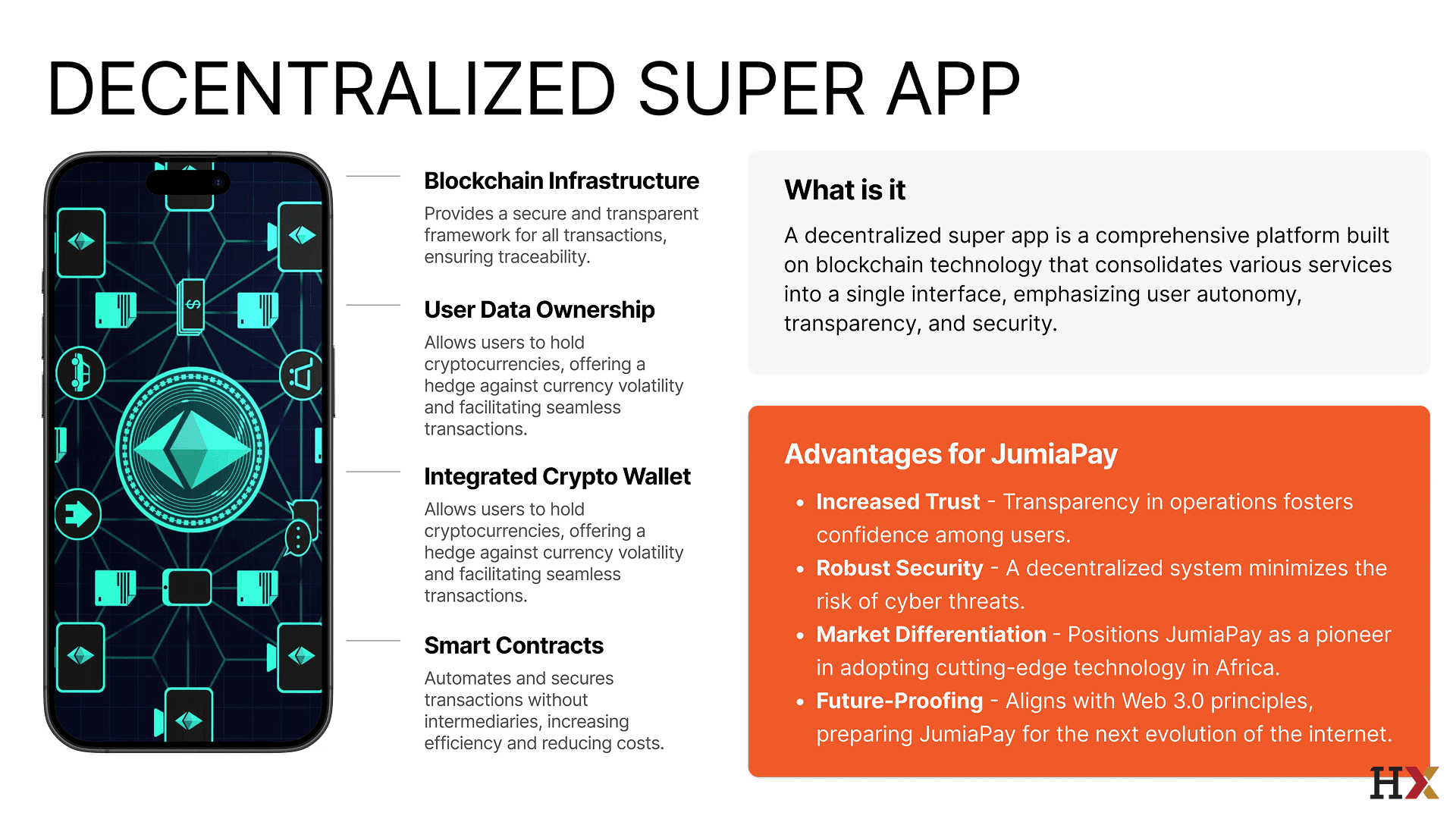

Decentralizing JumiaPay’s existing super app infrastructure will further enhance its capabilities. This move will democratize finance across the continent by allowing users greater control over their financial data and transactions. By integrating blockchain technology, JumiaPay can push the boundaries of traditional financial institutions, setting new industry standards while championing customer needs. This strategy could position JumiaPay at the forefront of Africa’s decentralized financial ecosystem in the emerging web-3 world.

Proposed Plan of Action

This section builds upon the recommendation to decentralize their super app. It outlines the rationale behind the proposal, supporting evidence and trends, and an analysis of potential pitfalls along with strategies for mitigation.

The decentralized finance (DeFi) market has grown exponentially — from $1 billion in 2019 to over $80 billion in 2021 (Johnson, 2021, p. 23) — indicating a significant shift towards decentralized financial solutions. For Jumia, this presents an opportunity to leverage blockchain infrastructure to provide a secure and transparent framework for all transactions. By adopting this infrastructure, JumiaPay can enhance trust among previously risk-averse customers, empowering users through greater control over their personal and financial data. This aligns with the increasing consumer demand for privacy and data ownership.

Driving Financial Inclusion

The potential for JumiaPay to drive further financial inclusion in Africa would also become more significant. By offering a decentralized super app, JumiaPay can provide unbanked populations with access to secure and transparent financial services. This aligns with the broader goal of increasing financial inclusion across the continent and addressing the needs of underserved communities.

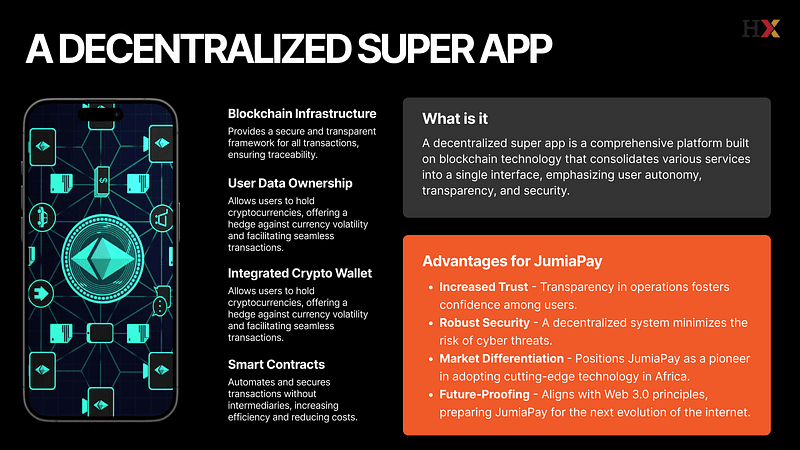

Key Features of the Super App

A decentralized super app will incorporate several key features that can transform JumiaPay’s service offerings:

Blockchain Infrastructure: Ensures traceability and security for all transactions. This transparency is crucial in building consumer confidence.

Integrated Crypto Wallet: Allows users to hold cryptocurrencies; this feature not only offers a hedge against currency volatility — a pressing concern in many African economies — but also facilitates seamless transactions across various currencies.

Smart Contracts: Automate and secure transactions without the need for intermediaries. This innovation can significantly increase operational efficiency and reduce costs.

Implementation Strategy

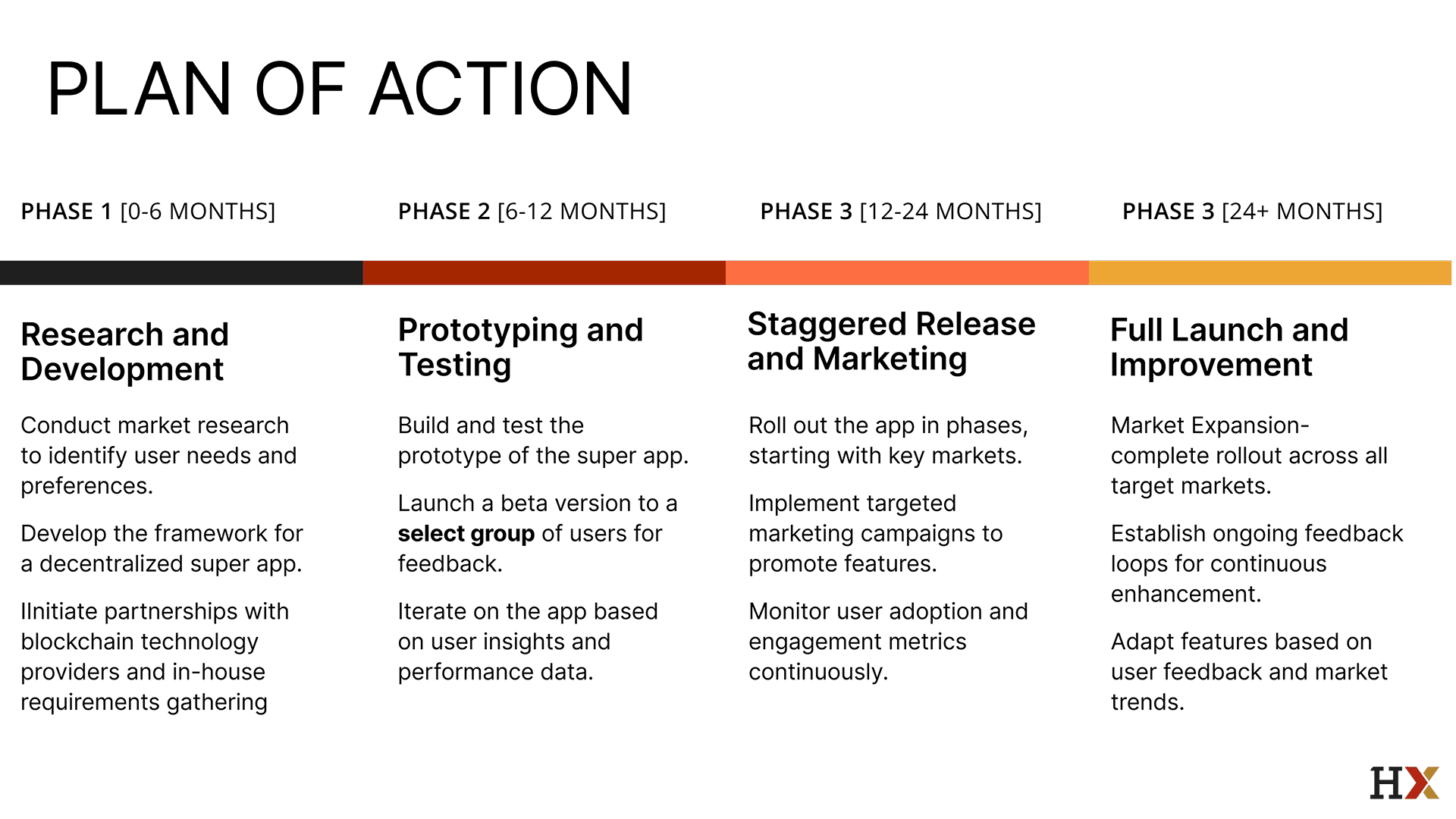

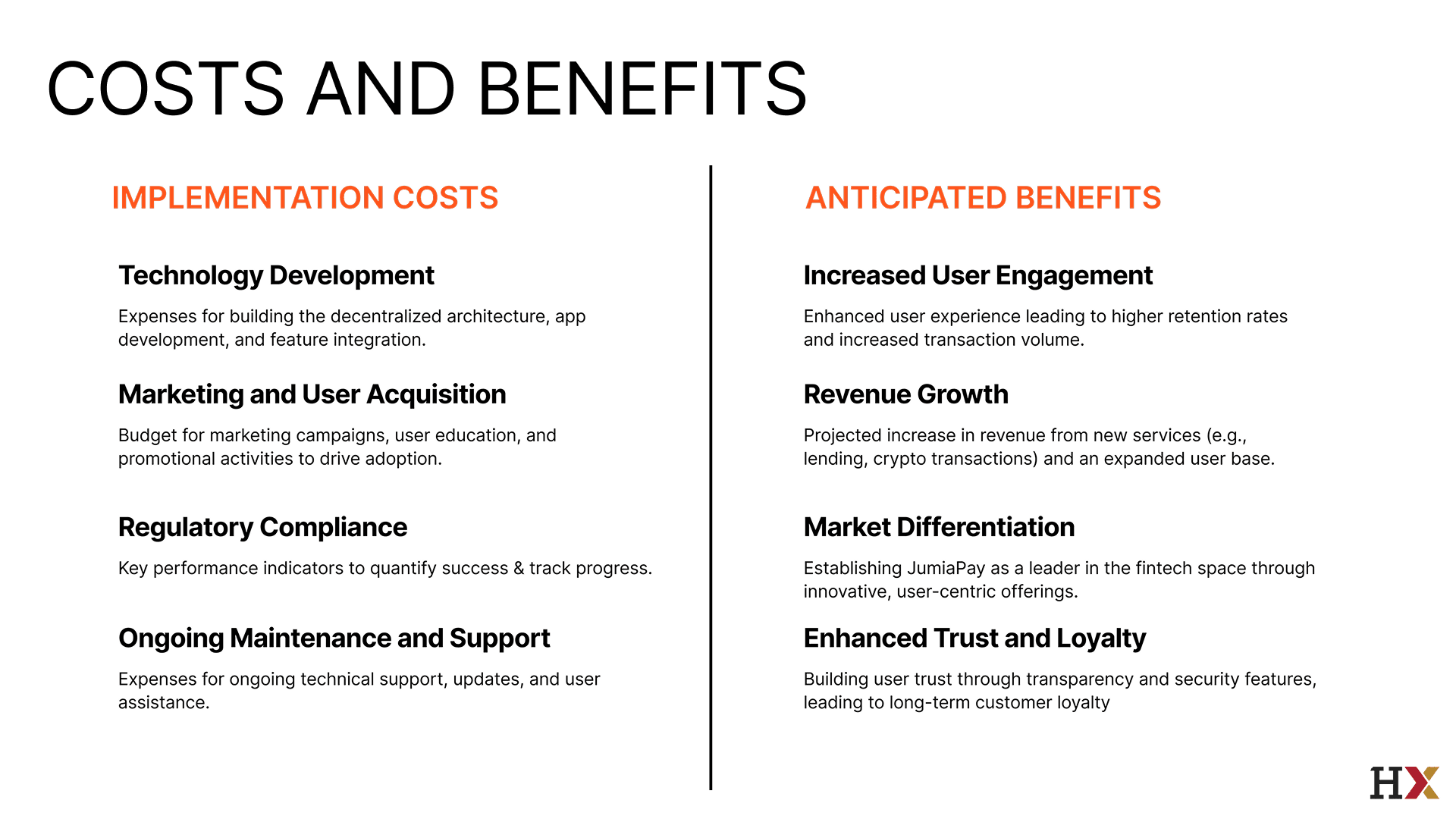

While the benefits of adopting such advanced technology are compelling, it is essential to recognize the associated risks. Therefore, the implementation strategy must be cautious and methodical. A phased approach is recommended to maximize adoption and provide JumiaPay with the necessary space to test and iterate on the app’s features.

Phase 1: Research: This stage will involve comprehensive market research to refine the app’s features and user interface. Engaging with stakeholders — including users, advisors, and regulators — will be crucial to gather insights around proposed changes.

Phase 2: Development: Focus on feature definition, user interface design, prototyping, and testing. This iterative process will ensure that the app meets user needs.

Phase 3: Rollout: The release should coincide with an education-focused go-to-market strategy that communicates enhanced security features and commitment to user control.

A survey by PwC found that 77% of consumers in Africa prefer platforms that offer transparency and data ownership (PwC, 2022, p. 30), indicating a strong market for decentralized solutions.

Addressing Challenges

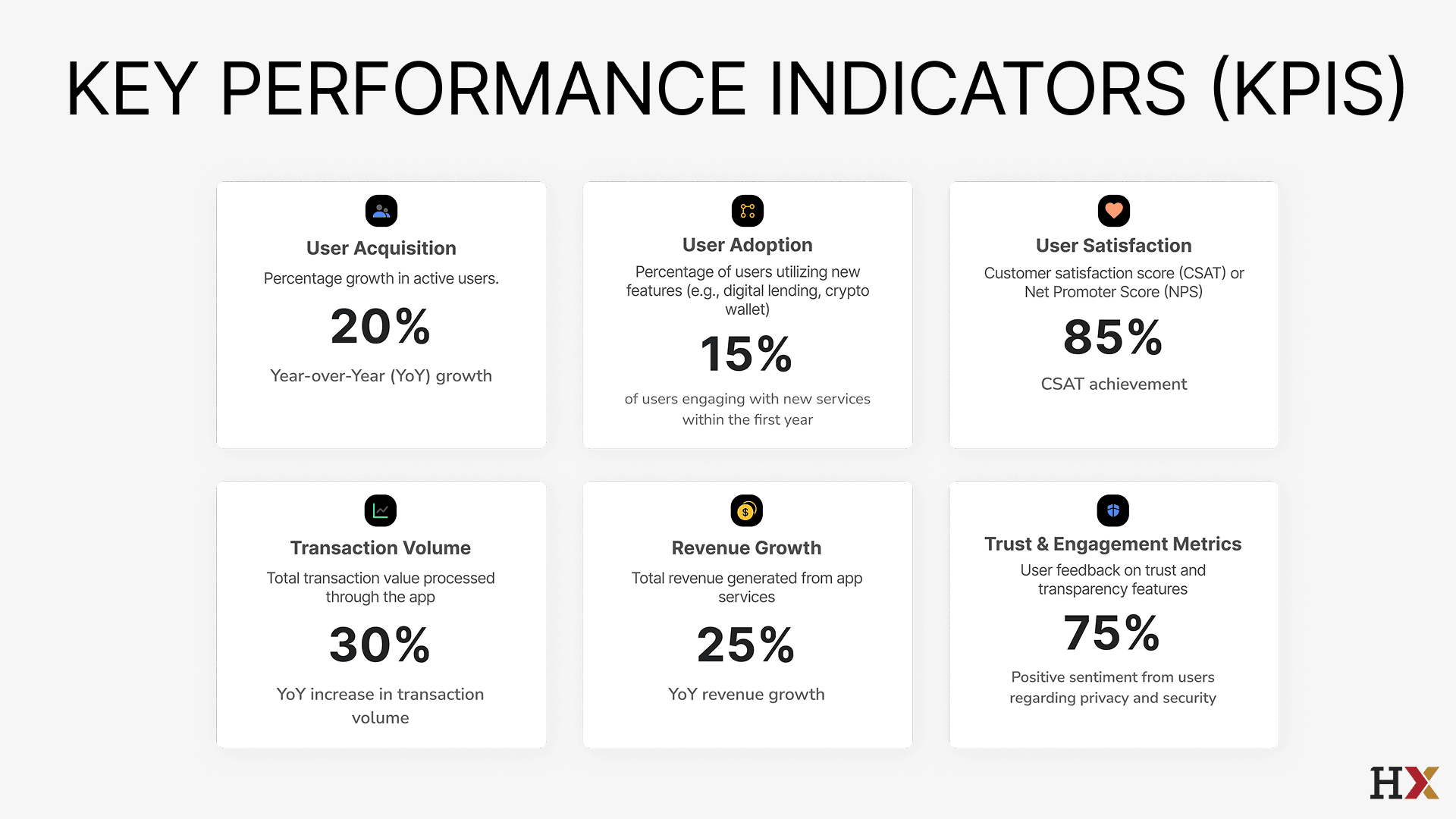

As we move towards the full launch of the app, it is important to address potential challenges proactively. The success of execution will be critical; establishing key performance indicators (KPIs) will help track progress focusing on user acquisition, satisfaction, transaction volume, and revenue growth.

Regulatory compliance will be a primary focus throughout the implementation process. Early engagement with regulators for approvals will be essential to navigate complex legal landscapes. Building user trust is another significant challenge; therefore, early educational campaigns could be key. Unforeseen technical challenges can be mitigated through best development practices and partnerships with experienced experts in the field.

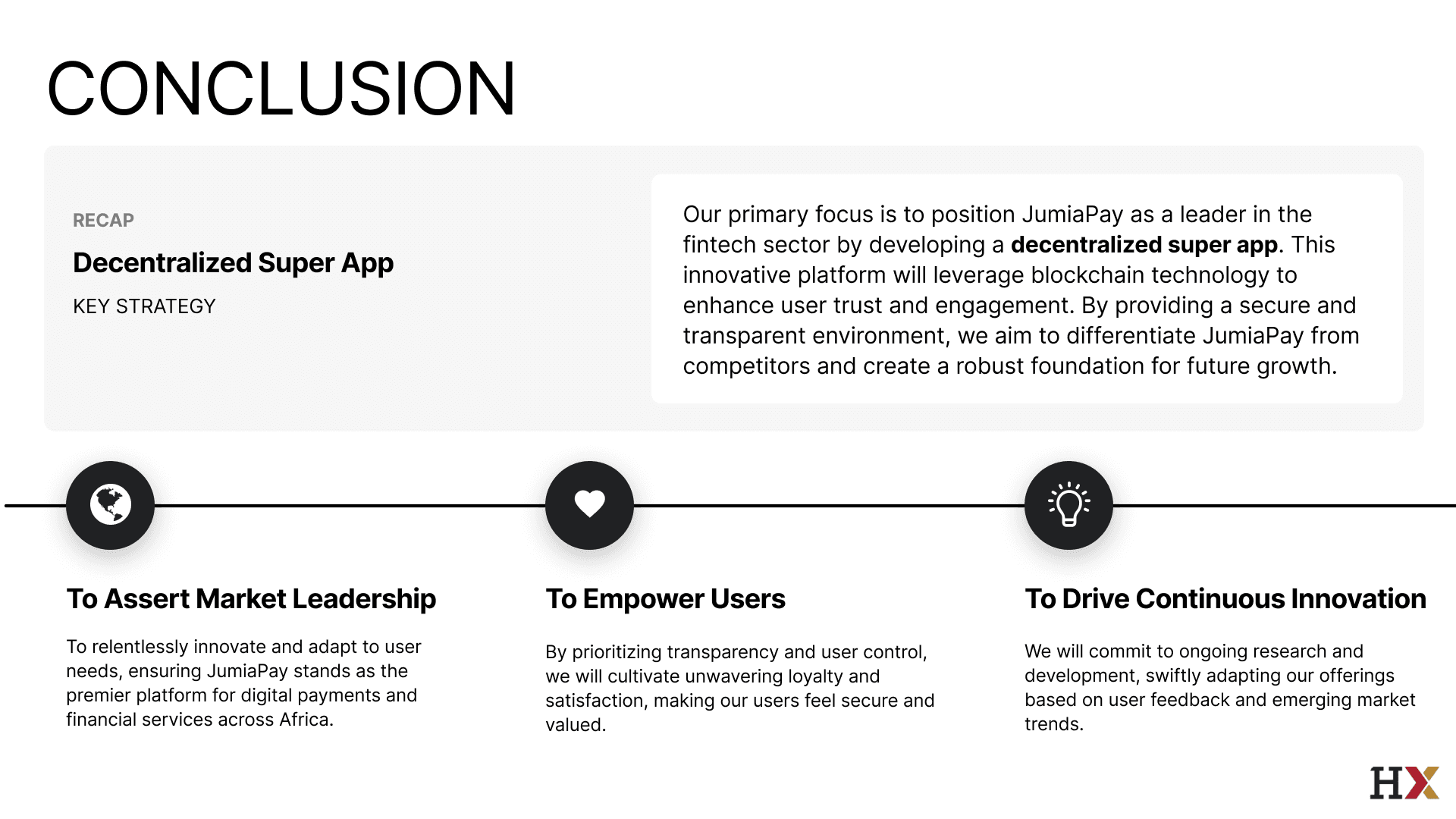

Conclusion

JumiaPay faces a complex set of challenges in the rapidly evolving fintech landscape — diverse economic conditions across multiple nations and shifting customer sentiment are among them. Given JumiaPay’s potential to contribute to the fintech revolution and enable financial inclusion through decentralization represents a vital step toward democratizing finance. This move pushes traditional financial institutions’ boundaries while setting new industry standards that champion customer needs.

The proposed solution incorporates key features such as blockchain infrastructure, integrated crypto wallets, and smart contracts — positioning JumiaPay for success through a phased implementation strategy. By leveraging existing partnerships while proactively addressing regulatory compliance issues; JumiaPay can transition effectively into this innovative platform.

This strategic move not only addresses current market needs but also sets up future growth opportunities — solidifying JumiaPay’s leadership role in Africa’s fintech revolution while promoting financial inclusion that ultimately transforms millions of underserved individuals’ financial landscapes.

Summary Deck:

References

Doe, J. (2021). The Rise of E-commerce Giants in Africa. New York: HarperCollins.

Johnson, M. (2021). Decentralized Finance: The Future of Financial Systems. London: Routledge.

JumiaPay (2023). Quarterly Financial Report Q2 2023. Retrieved from [JumiaPay website].

Lee S., (2020). Global Fintech Innovations: Case Studies and Trends. Singapore: Springer.

PwC (2022). Consumer Preferences in African Fintech. PwC Research Reports.

Smith A., (2022). Digital Transformation in Africa: Opportunities and Challenges. Boston: MIT Press.